Memory shortage, rising consumer prices, and the issuing stack's modernization imperative

AI-driven memory scarcity is already pushing consumer hardware prices higher—forcing banks and issuers to choose between modernizing their origination and decisioning infrastructure or ceding the financing layer to faster competitors.

Subscriber · Sign in to listen to the audio briefing

Audio briefings are available to subscribers. Sign in with the email you used to subscribe — we'll send a one-time code.

Reading Micron, Apple, and Klarna together, this week's tape tells a bigger story than one strong earnings call, one pressured hardware name, and one BNPL stock ticking higher.

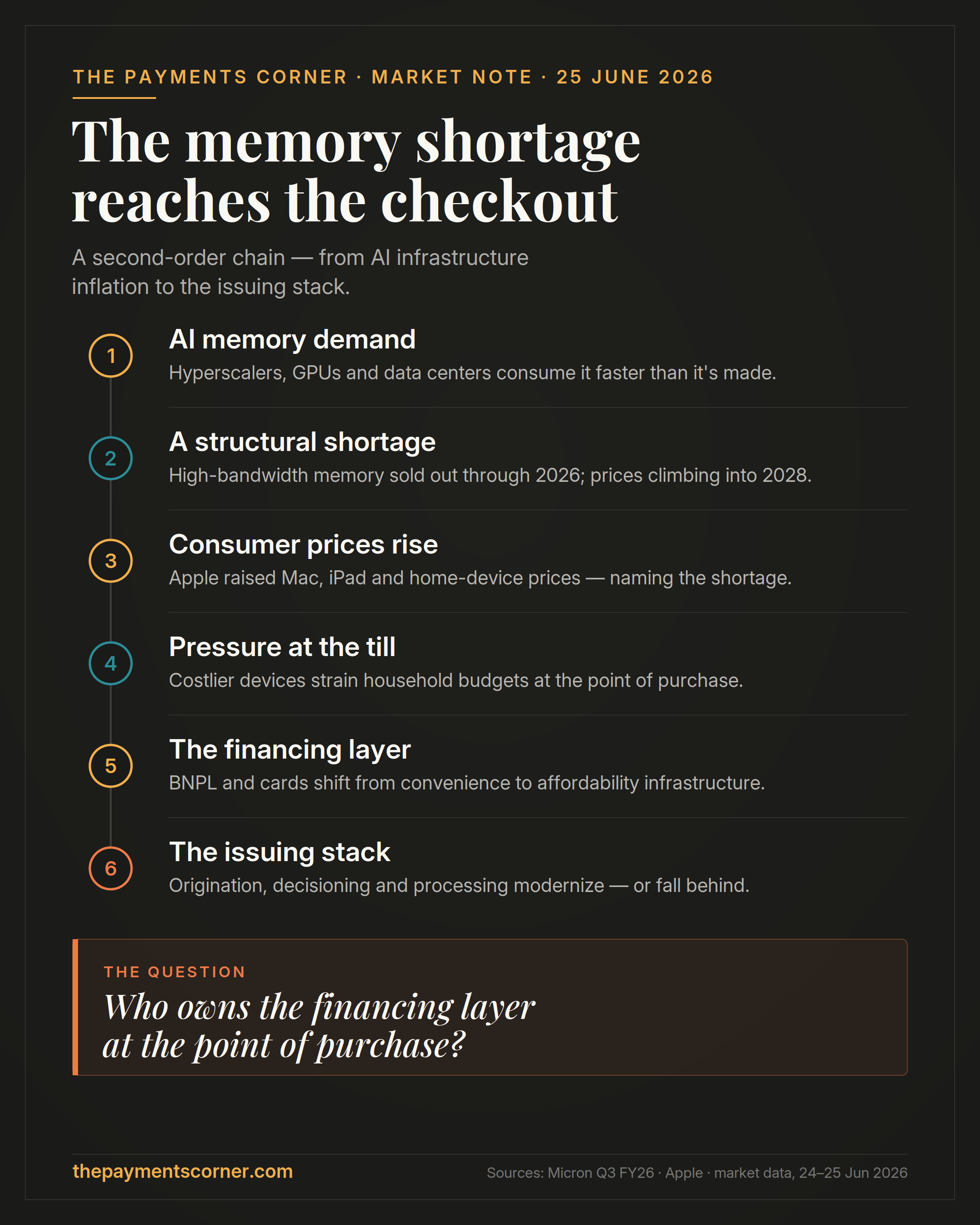

Micron's results did more than validate AI infrastructure demand. They confirmed that **memory has become a strategic constraint** — high-bandwidth memory sold out through 2026, record margins, and a shortage management expects to persist into 2028.

The same demand curve powering hyperscalers, GPUs, and data centers is now reaching into the economics of laptops, tablets, and phones. Micron was explicit that the squeeze reaches consumer devices — not just the data center.

**This week, that stopped being a forecast.**

On June 25, Apple raised prices across Macs, iPads, and home devices — and named the cause: an unprecedented memory and storage shortage driven by AI. The stock fell 6.1% to close the day. The downstream cost flow everyone has been modeling didn't arrive next quarter — it arrived in a price increase.

Which is what makes Klarna worth watching.

If consumer hardware — and eventually more of the basket — grows more expensive, BNPL stops being a checkout convenience and starts looking like an affordability layer in retail commerce. Not because consumers want more debt. Because merchants need flexible payment options to protect conversion, basket size, and retention in a higher-price environment.

For banks, issuers, networks, fintechs, and merchants, the question sharpens:

If AI infrastructure inflation pushes consumer prices higher, who owns the financing layer at the point of purchase?

That question doesn't only separate BNPL from cards. **It separates the issuers who can move from the ones who can't.**

A higher-price environment raises consumer demand for new capabilities — faster origination, smarter decisioning, more flexible processing — at the exact moment many issuers still run on stacks that were never built to deliver them. The institutions that modernize origination, decisioning, and processing will set the pace. The ones anchored to legacy infrastructure will spend the next cycle reacting to it.

Memory inflation, in other words, doesn't stop at the device. It eventually lands as pressure on the issuing stack.

The memory shortage looks like a semiconductor story. Its second-order effects may surface across payments, credit, issuing, BNPL, merchant acquiring, and consumer finance.

That's the part worth paying attention to.

Franco Di Pietro

The Payments Corner

30+ years across payments, fintech, banking, and financial infrastructure. Operator-level perspectives on the systems that move money.

Related Insights

BNPL Sits Directly in the Gap Between Consumer Behavior and Traditional Credit Models

BNPL sits directly in the gap between how consumers experience credit and how institutions traditionally model it. The consumer-side behavioral pattern is consistent and well-documented. But the issuer-side value proposition is discussed far less often — even though it may be just as important.

BNPL Didn't Arrive Late in the U.S. — The Conditions Arrived Late

BNPL didn't arrive late in the U.S. — the conditions arrived late. I've been familiar with installment-based credit since the early 1990s, working across Brazil and Mexico. The traditional U.S. revolving-credit model functioned effectively for decades, until the surrounding economic conditions began changing materially.

BNPL Isn't a Checkout Feature. It's Credit.

BNPL is often discussed as a checkout experience or a UX innovation. But increasingly, the market is beginning to price it for what it fundamentally is. Credit. Yesterday's market activity, paired with New York's proposed regulatory framework, reinforced that distinction clearly.