Insights

The Payments Corner · Ecosystem access

Three layers of access

Operator-level analysis on payments infrastructure, embedded finance, credit systems, and the AI-assisted synthesis layer shaping the ecosystem. Enter at the layer that fits how you read.

I· Open Access

Open Access

The public reading experience. No signup required.

- Insights & analysis

- Latest Ecosystem Pulse briefing

- Research previews

Open to all readers.

II· Premium

Premium

The full intelligence stack — for people who work in the space.

- Full Markets intelligence suite

- Full Signals stream

- Friday Ecosystem Digest

- Per-category intelligence feeds

$7.00/mo or $70/yr (2 months free).

Open now · free through July 31.

III· Subscriber

Subscriber

Inside the ecosystem. Free newsletter participation.

- Full research reads + audio briefs

- Weekly editorial briefing

- Audio briefings archive

No paid subscription required.

Featured

Research · Latest

Research Article

Research ArticleResearch12 MIN READ · 2,290 WORDS · 10 SECTIONS

Measuring Payments Cohort Cohesion: A Market-Adjusted Methodology

The quantitative methodology behind the cohesion read the Pulse reports each week: market-adjusted residual correlation, a leave-one-out reclassification test, and a full accounting of where the method fails.

Audio BriefListen to this research

Latest

All Research

ResearchJUL 28 · 2026

Not a watchlist of stocks. A map of how payments makes money — and a way to watch that map redraw itself.

The Payments Corner

Payments Infrastructure·

A Map, Not a Portfolio

The methodology behind the 50 TPC Payments Index — the reasoning that turns fifty tickers into an instrument for reading the payments ecosystem, and the discipline that keeps it from becoming a watchlist.

Audio BriefListen

Franco Di Pietro · Research

ResearchJUL 21 · 2026

The central question is not whether more value can be created from debit. It is who captures it.

The Payments Corner

Research·

Debit After Durbin: Rewards, Routing, and the Search for Lost Economics

Fifteen years after Durbin capped debit interchange, the value it displaced migrated across the household wallet. As network ownership emerges as an issuer strategy, the unsettled question returns: who captures the value?

Audio BriefListen

Franco Di Pietro · Research

ResearchJUL 07 · 2026

The law is not hostile to stablecoin loyalty. It is hostile to stablecoin savings wearing loyalty's name.

The Payments Corner

Stablecoins·

A Reward, or Interest? The Loyalty Question Deciding Stablecoin Law

Part I of a two-part research program. The Senate's market-structure bill is stalled, in part, over a definition the payments industry settled decades ago.

Audio BriefListen

Franco Di Pietro · Research

Featured

Insights · Latest

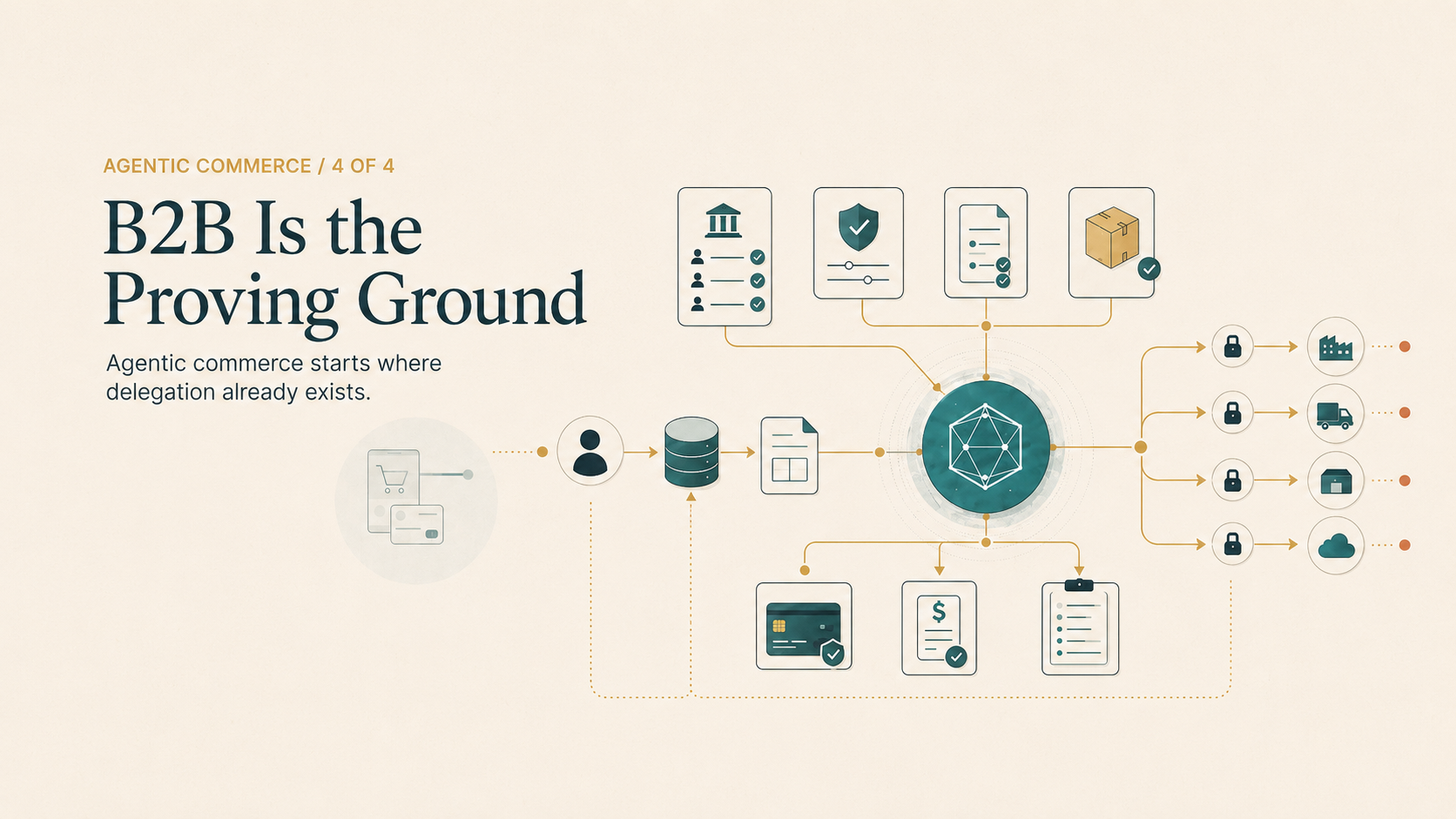

Agentic CommerceAugust 6, 2026 ·

Featured Insight

The B2B Proving Ground — Agentic Commerce (4 of 4)

The first durable agentic volume won't come from the shopping cart. It'll come from the back office.

Audio BriefListenListen to the operator-level summary

Franco Di Pietro · InsightBy Franco Di Pietro · Insight

Latest

All Insights

SignalJUL 30 · 2026

The venue moved from Congress to the Comptroller. The line didn't move at all.

The Payments Corner

Crypto·

The CLARITY Fork Is Bending Toward the Regulators

An interim marker between the two parts of the stablecoin-rewards research. The Senate probably won't move CLARITY before recess — which tips the reward/interest fight toward the OCC track, the slower path to the same line.

Audio BriefListen

Franco Di Pietro · Insight

SignalJUL 24 · 2026

Tokenization began as a way to protect sensitive account information.

The Payments Corner

Payments Infrastructure·

Tokenization: From Security Layer to Checkout Platform

Tokenization began as a way to protect sensitive account information. Today, it is becoming the platform layer connecting credentials, wallets, checkout, and the customer experience.

Audio BriefListen

Franco Di Pietro · Insight

SignalJUL 23 · 2026

Issuers face a fork: be the passive endpoint of an agent's decision, or the layer that governs it.

The Payments Corner

Agentic Commerce·

Top of Permission — Agentic Commerce (3 of 4)

Issuers face a fork: be the passive endpoint of an agent's decision, or the layer that governs it.

Audio BriefListen

Franco Di Pietro · Insight

Markets · Curated intelligence

View Market WatchWhere the payments stack stands today.

Five layers of the public payments universe, summarised at today's close. Click through for the full ticker table.

Signals

Signals From the Ecosystem

Curated developments across payments, banking technology, policy, and financial infrastructure — interpreted through an operator lens. View all →

Trade Press

Digital Transactions

August 2026

Western Union embedding stablecoin rails into a card-linked wallet forces a structural reckoning for remittance corridors: if stablecoin settlement displaces correspondent banking legs, the interchange and FX spread economics that incumbents depend on compress materially. Operators running cross-border infrastructure need to treat this as a live architecture shift, not a product experiment.

Trade Press

Finextra — all headlines

August 2026

Trade Press

PaymentsJournal

August 2026

Trade Press

PaymentsJournal

August 2026

Fintech

Tearsheet

August 2026

Loyalty

Antavo

July 2026

Financial Press

MarketWatch

August 2026

Loyalty

Antavo

July 2026

Trade Press

PYMNTS

August 2026

Trade Press

PYMNTS

August 2026

WhitepapersAll whitepapers

Formal, deeply-sourced research deliverables — downloadable PDFs on payments infrastructure, credit evolution, and financial technology.

Featured

20 PP · PDF

Whitepaper · Community Finance The Payments Corner

The Payments Corner

The Future of Community Finance

Community FinanceJanuary 2026

The Future of Community Finance

Community banks and credit unions remain structurally important, but the economics, technology stack, and customer expectations that defined the franchise for the last half-century are being re-priced in real time. The next era will belong to institutions that combine local trust with platform-grade infrastructure.

20 PAGES · PDF · 16-MIN READRead the paper

Credit InfrastructureMarch 2026

BNPL and Modern Credit Architecture

Whitepaper · Credit Infrastructure

BNPL and Modern Credit Architecture

How Fintechs, Embedded Credit, and Transaction-Level Decisioning Are Rewiring Consumer Finance

Franco Di Pietro · The Payments Corner Research

Buy Now, Pay Later is often treated as a consumer payment trend, a checkout conversion tool, or a credit-card alternative. That framing is too narrow. BNPL is better understood as the visible edge of a deeper architectural shift in consumer finance: credit is moving from static, account-level products toward contextual, transaction-level, embedded, and data-informed credit orchestration. This shift did not begin in the United States. BNPL matured earlier in markets such as Sweden, Australia, and the United Kingdom, where different consumer-credit habits, ecommerce dynamics, debit usage, fintech adoption, and regulatory boundaries created more open space for alternative installment products. The U.S. market evolved later, not because consumers lacked interest in installment credit, but because the credit card already served as a powerful incumbent architecture: universal acceptance, revolving credit, rewards, fraud protection, disputes, chargebacks, credit reporting, and merchant connectivity were already deeply embedded. The late U.S. arrival is strategically important. BNPL is now entering a market with mature card infrastructure, large bank issuers, network economics, entrenched rewards behavior, sophisticated credit bureaus, and heightened regulatory scrutiny. The U.S. BNPL story is not simply about fintech growth. It is about whether banks, credit unions, processors, networks, merchants, and fintech platforms can adapt to a credit environment where the unit of decisioning is increasingly the transaction.

Page 1 · 15

How Fintechs, Embedded Credit, and Transaction-Level Decisioning Are Rewiring Consumer Finance

Buy Now, Pay Later is often treated as a checkout conversion tool. That framing is too narrow. BNPL is better understood as the visible edge of a deeper architectural shift: credit moving from static, account-level products toward contextual, transaction-level, embedded orchestration.

Page 2 · 15

Preview · pages 1–2 of 15Read the paper

Cooperative FinanceFebruary 2026

The Cooperative Advantage

Whitepaper · Cooperative Finance

The Cooperative Advantage

Why Credit Unions Are Winning the Battle for the Modern Consumer

Franco Di Pietro · The Payments Corner Research

The U.S. consumer financial services market is entering a structural reset. Federally insured credit unions now represent a systemically meaningful segment of U.S. finance, with approximately $2.43 trillion in assets, $1.72 trillion in loans outstanding, and 144.7 million members at year-end 2025. The sector generated $18.8 billion in net income in 2025, up 31.5 percent from the prior year, even as the number of federally insured credit unions continued to decline. This combination — larger aggregate scale, stronger earnings, and fewer institutions — signals that the cooperative system is not simply growing; it is consolidating into more capable, more technology-enabled platforms. This paper argues that credit unions are no longer competing only on price or affinity. Their advantage is increasingly architectural: a member-owned economic model that can recycle surplus into lower loan rates, higher deposit yields, fewer fees, and stronger member outcomes; a trusted relationship model; and a technology ecosystem that is narrowing the historical digital gap versus large banks. The future competitive question is whether credit unions can convert cooperative economics into primary financial relationships at scale through digital onboarding, real-time payments, modern credit products, data-driven lifecycle engagement, and disciplined consolidation.

Page 1 · 11

Why Credit Unions Are Winning the Battle for the Modern Consumer

The U.S. consumer financial services market is entering a structural reset. Credit unions are no longer competing only on price or affinity — their advantage is increasingly architectural: a member-owned economic model translating cooperative economics into modern infrastructure.

Page 2 · 11

Preview · pages 1–2 of 11Read the paper

Short Videos

Quick insights, explained clearly

Bite-sized videos breaking down complex payments topics in minutes — across LinkedIn, Instagram, YouTube, and TikTok.

06 live

01 live

Coming soon

Instagram brief in production.

Coming soon

Instagram brief in production.

Coming soon

Instagram brief in production.

Coming soon

Instagram brief in production.

Coming soon

Instagram brief in production.

YouTube

Coming soon

Coming soon

YouTube brief in production.

Coming soon

YouTube brief in production.

Coming soon

YouTube brief in production.

Coming soon

YouTube brief in production.

Coming soon

YouTube brief in production.

Coming soon

YouTube brief in production.

TikTok

Coming soon

Coming soon

TikTok brief in production.

Coming soon

TikTok brief in production.

Coming soon

TikTok brief in production.

Coming soon

TikTok brief in production.

Coming soon

TikTok brief in production.

Coming soon

TikTok brief in production.

Follow for more insights

— From Inside the Stack

An editorial platform on the modern payments stack

The Payments Corner covers payments infrastructure, credit systems, embedded finance, issuer processing, and the intelligence layer reshaping the modern stack.

Coverage sits beneath the headlines: rails, settlement finality, decisioning systems, and the modernization pressure on incumbent processors, core vendors, and the institutions building around them.

The platform operates across formats — short-form video, long-form research, audio briefings, a weekly editorial cadence, and a curated stream of ecosystem signals. Each surface is authored from inside payments rather than alongside it, grounded in how the systems behave at scale rather than how vendors describe them.