A Reward, or Interest? The Loyalty Question Deciding Stablecoin Law

Part I of a two-part research program. The Senate's market-structure bill is stalled, in part, over a definition the payments industry settled decades ago.

Subscriber · Sign in to listen to the audio briefing

Audio briefings are available to subscribers. Sign in with the email you used to subscribe — we'll send a one-time code.

This is Part I of a two-part research program, published deliberately in two stages because the situation it analyzes is live. Part I makes the argument that can be made today — before the Senate acts on the legislation at the center of it. Part II, the full treatment, publishes once Washington has decided, in whichever direction it decides.

The most consequential question in payments law this summer sounds almost trivial: what is the difference between a reward and interest?

The question is not academic. The Senate's crypto market-structure bill — the CLARITY Act, the legislation meant to give digital assets their full American rulebook — missed its informal July 4 signing target and sits on the Senate calendar with no floor vote scheduled.1 The chamber returns from recess on July 13 with roughly three working weeks before the August break, the window that policy analysts have consistently identified as the last realistic gate for passage this year.2 Three disputes stand between the bill and the sixty votes it needs. One of them is the definition of a stablecoin reward.

A trillion-dollar market's rulebook is hung up, in part, on a loyalty question. And the striking thing, for anyone who has spent time inside payments, is that the industry answered this question decades ago — without legislation, without litigation, and so cleanly that almost nobody noticed a line was being drawn at all.

What the GENIUS Act built, and the door it left open

The GENIUS Act, signed in July 2025, gave payment stablecoins their first federal framework. Its architecture rests on a single premise: stablecoins are payment instruments, not deposit substitutes. They exist to move value, not to store it at a return. To defend that premise, the statute prohibits permitted stablecoin issuers from paying interest or yield to holders.3

The prohibition was written narrowly. It binds issuers. It says far less about the exchanges, wallets, and affiliates who actually hold the customer relationship — the distribution tier of the stablecoin stack. That silence became the story.

Within months, the largest distribution platforms were paying holders a rate on stablecoin balances and describing the payment as a loyalty reward. The mechanics are straightforward: reserve income earned on the assets backing a stablecoin flows to the issuer, a revenue-sharing arrangement moves a portion of it to the distributing platform, and the platform passes value through to customers as a balance-linked rewards rate. The issuer pays no yield. The holder earns one anyway. The most prominent such program has paid holders 3.5 percent on balances held in-app — more recently repositioned behind a paid subscription tier, without changing the underlying balance-linked mechanic — an arrangement its operator books as a reward rather than interest, and one that contributed to stablecoin-related revenue of roughly $305 million in a single quarter.4

The scale is no longer marginal. At roughly $300 billion of stablecoins outstanding, a rewards rate of 1.5 to 2.5 percent implies an annual incentive pool in the range of $4.6 to $7.7 billion — and multiples of that under the supply forecasts that project the market toward the trillions by 2030.5

The banking industry regards this as the exception swallowing the rule. A Treasury advisory analysis identified some $6.6 trillion in transactional deposits as exposed if stablecoins can offer deposit-like returns, and community banks in particular have warned that balance-linked rewards siphon the deposits that fund local lending.3 Trade groups from the American Bankers Association to the Bank Policy Institute have spent the past year pressing Congress and regulators to extend the prohibition beyond issuers to any affiliate or intermediary that delivers yield in practice.6

The machinery now in motion

Two processes are now testing where the line falls, on parallel tracks.

The first is regulatory. In February 2026 the Office of the Comptroller of the Currency — designated by the GENIUS Act as the primary federal stablecoin regulator — proposed implementing rules that would reach past the issuer. The proposal establishes a rebuttable presumption: where an issuer and an affiliate or related third party have coordinated arrangements that result in yield paid to holders in connection with holding a stablecoin, the arrangement is treated as prohibited unless the parties can prove otherwise.7 The design inverts the burden of proof, and legal analyses were quick to note its breadth — any economic arrangement tying holder rewards to stablecoin balances is potentially captured.8 The comment period closed May 1, with the banking trades arguing for the broadest possible reading and the digital-asset industry arguing that Congress deliberately banned issuer yield while leaving platform rewards lawful.

The second track is legislative, and it is where the definition is being written most explicitly. The CLARITY Act text that emerged from months of negotiation restricts the payment of interest or yield "solely in connection with the holding" of payment stablecoins, or on a stablecoin balance "in a manner that is economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit."9 The Senate Banking Committee advanced the bill 15–9 in May.10 The compromise principle underneath the language is legible: value paid for holding is prohibited; value earned through activity survives. The crypto industry's own characterization of the deal is that rewards are permitted when stablecoins are spent.11

The banks want the line tighter still, and said so the day the bill advanced — urging that interest-like rewards for holding be prohibited outright while "certain payment stablecoin transactions and activities" remain able to generate rewards.12 Note what both sides of that sentence concede: everyone now accepts that the distinction runs between balances and transactions. The remaining fight is over how much ambiguity survives in the middle.

The taxonomy loyalty solved decades ago

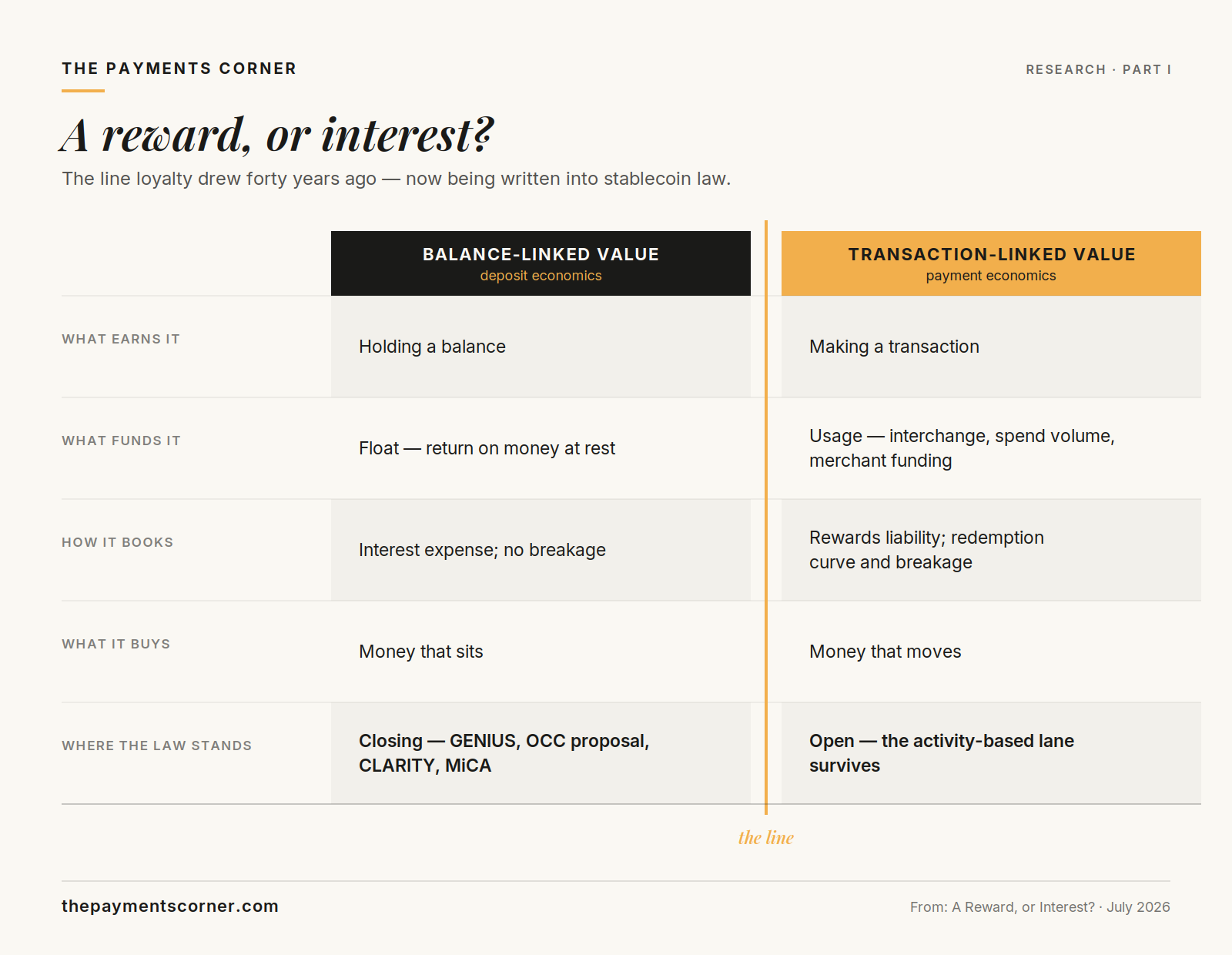

Here is what makes the dispute remarkable to a payments audience: this line is not new. It is the oldest line in loyalty.

Card rewards have existed at scale since the 1980s, and in four decades no regulator, court, or customer has seriously confused two percent cash back with interest. That is not because the sums are small — U.S. card rewards run to tens of billions of dollars a year — but because of a single design choice made at the category's birth: rewards are earned on transactions, not balances.

The distinction is structural, and it shows up everywhere in how a loyalty program actually runs.

Consider the funding. Card rewards are financed by the economics of usage — interchange on the transaction, merchant co-funding, the margin generated when the product moves. Deposit interest is financed by float: the return earned on money at rest. A rewards program's cost scales with activity; an interest expense scales with balances. These are different businesses with different unit economics, and any program manager can tell you which one they are running by looking at a single line of the P&L.

Consider the accounting. Rewards accrue as a liability against future redemption, they carry breakage — the fraction of earned value that is never claimed — and they are managed as a marketing expense that shapes behavior. Interest carries no breakage and shapes nothing; it simply compensates the depositor for parking funds. A points liability with an actuarial redemption curve is not a deposit obligation, and the two have never been booked alike.

Consider, finally, the behavior each one buys. Rewards paid on spend make money move faster: they pull volume toward a product at the moment of use. Returns paid on balances make money sit still: they compete for the deposit. One accelerates payments; the other competes with banking.

And federal law has already ratified this taxonomy — twice, in venues far from crypto. The first is tax law. The IRS has for decades treated card rewards earned on spending as rebates — adjustments to the purchase price, not income to the cardholder — while interest is, unambiguously, taxable income. Two forms of value flowing to the same customer from the same institution, and the tax code has never confused them, because one is priced against a transaction and the other against a balance. The second ratification came as a natural experiment. When the Durbin amendment capped debit interchange for large issuers in 2011, debit rewards programs were discontinued across large issuers in short order. Nothing about deposit balances had changed — only the usage economics had been capped, and the rewards funded by them evaporated on cue. It is difficult to imagine cleaner empirical proof that rewards are a function of transaction economics, not of money at rest. If they were interest in disguise, capping interchange would not have killed them.

That is the entire dispute, stated in loyalty terms. Balance-linked value is deposit economics. Usage-linked value is payment economics. The line that card programs have respected for forty years without anyone legislating it is now being written, almost verbatim, into federal law — "economically or functionally equivalent" to deposit interest is a statutory rendering of a distinction every loyalty operator already runs a business on.

The ghost of Regulation Q

There is also a longer American history here, and it explains why the drafters reached for equivalence language rather than a simple ban.

The United States has prohibited interest on transactional money before. Regulation Q, born of the Banking Act of 1933, barred interest on demand deposits for nearly eighty years — on a rationale that rhymes with the GENIUS Act's: money meant for payments should not be competing on yield. What followed was one of the great cat-and-mouse games in financial history. The prohibition did not eliminate the economics; it drove them into engineering. NOW accounts reproduced interest-bearing checking under another name. Sweep programs moved balances out of demand deposits each night and back each morning. Money market funds rose, in meaningful part, as a yield-bearing substitute for the deposits Regulation Q had frozen. Each workaround was formally compliant and economically equivalent, and regulators spent decades chasing the difference until the prohibition was finally repealed in 2011.

The lesson was evidently learned. The CLARITY Act's operative phrase — value paid "in a manner that is economically or functionally equivalent" to deposit interest — is Regulation Q's institutional memory written into a statute at birth. Congress is not banning a payment; it is banning an economic function, however labeled. That is precisely why the reward-versus-interest definition carries so much weight, and why "we call it a loyalty program" was never going to be a durable answer. The last eighty years taught American financial law to look through the name to the economics — and the economics of a balance-linked rate are, and have always been, interest.

The same conclusion has been reached abroad. Europe's MiCA framework prohibits interest on e-money tokens on the same payment-instrument logic, which means both major Western regimes are converging on the identical line. For global program designers, there is no jurisdiction to arbitrage toward: value attached to holdings is closing everywhere; value attached to activity is the lane that remains open.

The design brief

Read that way, the legislative text stops being a compliance problem and becomes what it functionally is: a design brief for stablecoin loyalty.

The balance-linked version — hold coins, collect a rate — is living on borrowed time. Whether the end arrives through the OCC's presumption, the CLARITY Act's equivalence language, or a future Congress closing the gap outright, every institutional signal points the same direction, and the affected platforms have already begun restructuring their programs in anticipation.4

What replaces it will look strikingly familiar to anyone who has built card loyalty:

Earn on spend. Rewards attached to the payment event itself — a percentage of stablecoin transactions at participating merchants — sit squarely inside the activity-based safe harbor both chambers' language preserves. This is the cash-back model, re-platformed.

Earn on settlement. In B2B and cross-border flows, where stablecoins have their most credible payments case, incentives tied to settlement volume mirror the interchange-funded economics that have always financed commercial card rebates.

Merchant-funded offers. The most durable consumer loyalty has always been funded by the merchant seeking the sale, not by float. Card-linked offers translated to stablecoin rails carry no interest-equivalence exposure at all, because the value is unambiguously purchased behavior, not compensated holding.

Status and utility. Tier benefits, fee waivers, and access — the non-financial architecture of loyalty — were never within a mile of the prohibition and become relatively more valuable as the rate-based lever is removed.

One caution belongs in every design conversation: the safe harbor's edges are not yet fully drawn. The OCC's proposal prohibits yield paid in connection with the "holding, use, or retention" of a stablecoin without defining "use" — an omission legal reviewers flagged immediately, because it leaves open whether some transaction-tied incentives could be swept in alongside balance-linked ones.7 The prudent read for designers is a spectrum, not a switch: value priced against a specific payment event, funded by transaction economics, sits at the safest end; anything whose size tracks how much a customer holds, however the trigger is dressed, drifts toward the presumption. Programs should be built to survive an equivalence audit, not a labeling review — the Regulation Q lesson, applied prospectively.

There is a quiet irony in the regulatory outcome. By forcing rewards from balances to transactions, the law pushes stablecoins toward precisely what the GENIUS Act declared them to be: instruments that move rather than instruments that sit. The prohibition, properly implemented, is not hostile to stablecoin loyalty. It is hostile to stablecoin savings wearing loyalty's name — and in drawing that line it conscripts loyalty design into monetary policy.

Who runs stablecoin loyalty

If rewards must attach to usage, the interesting question becomes competitive: who is best positioned to operate them?

The exchanges hold the balances and the customer relationship, and they have proven willing to spend billions on incentives. But their programs were architected around holdings, their economics around reserve-income share — the exact structures under pressure. Rebuilding for activity-based rewards means acquiring capabilities exchanges have never needed: merchant networks, offer engines, redemption operations.

The issuers — meaning both stablecoin issuers and, more provocatively, the banks and card issuers watching from the incumbent side — know rewards economics cold. Forty years of managing earn rates, points liabilities, breakage curves, and co-brand partnerships is a directly transferable asset. A bank-issued stablecoin with transaction-linked rewards is, structurally, a debit rewards program on new rails, and no category of institution has more practice running one.

The merchants fund most of the loyalty economy today and have the strongest motive: stablecoin acceptance offers them a rail with materially different cost dynamics, and rewards are how consumer rails have always been seeded. Merchant-funded stablecoin incentives — spend-linked, category-specific, settlement-cheap — may be the configuration with the fewest legal questions and the clearest business case.

And the networks are the quiet fourth actor. Visa and Mastercard have spent two years building stablecoin settlement into their rails, and both operate loyalty and offer platforms at global scale. A network that can clear stablecoin transactions and orchestrate merchant-funded rewards across them holds the connective position it has always held in card loyalty — the switch through which usage-based value flows. If stablecoin rewards must attach to transactions, the entities that see the transactions are structurally advantaged.

The likeliest answer is a braid of all four. But the capability at the center of the braid — designing value that attaches to transactions, prices behavior, and survives an equivalence test against deposit interest — is a payments-industry competence, not a crypto-native one. The institutions that spent decades learning it did not expect it to become the decisive skill in stablecoin market structure. It has.

What to watch

Three weeks now matter more than the last twelve months. If the Senate moves the CLARITY Act before the August recess, the equivalence language — whatever its final tightness — becomes the operative federal definition of a stablecoin reward, and program redesign begins in earnest across the distribution tier. If the window closes, the OCC's rulemaking proceeds as the live venue, the presumption framework carries the weight the statute declined to, and the definitional fight migrates from legislative text to supervisory interpretation — a slower path to the same destination.

Either way, the direction of travel is set, and it was set long before Congress took up the question. The payments industry drew the line between a reward and interest at the birth of modern loyalty: value that moves money earns its keep; value that stills money is something else, and gets regulated like it.

Stablecoins are simply the newest rail to learn the oldest rule.

The law is not hostile to stablecoin loyalty. It is hostile to stablecoin savings wearing loyalty's name.

This is Part I of a two-part research program. Part II — the full treatment — publishes when the Senate acts, in whichever direction it acts: a section-level reading of the final statutory language or the OCC's operative rule, the industry's counter-case argued in full, the economics of the rewards pool under the surviving design space, and scenarios for how stablecoin loyalty gets built by exchanges, issuers, merchants, and networks. Part II will be available to Subscribers. Subscribe to be notified when it publishes.

Footnotes

-

CoinSpeaker, "CLARITY Act Stalls: Three Disputes Block Senate Vote," July 6, 2026. https://www.coinspeaker.com/clarity-act-senate-stall-crypto-regulation-2026/ ↩

-

Brian Gardner (Stifel), policy note on CLARITY Act timing, as reported by The Hill, "Obstacles threaten success of Clarity Act in Senate," May 20, 2026. https://thehill.com/policy/technology/5885518-clarity-act-senate-challenges/ ↩

-

Congressional Research Service, "The Stablecoin Yield Debate," updated March 2026. https://www.congress.gov/crs-product/IF13174 ↩ ↩2

-

Forbes, "The GENIUS Act Stablecoin Yield Ban Has a Coinbase-Shaped Hole," May 20, 2026. https://www.forbes.com/sites/digital-assets/2026/05/20/the-genius-act-stablecoin-yield-ban-has-a-coinbase-shaped-hole/ ↩ ↩2

-

CryptoSlate, "CLARITY Act stablecoin reward definition may split crypto's coalition," January 13, 2026. https://cryptoslate.com/clarity-act-stablecoin-reward-definition-may-split-cryptos-coalition-after-genius-yield-ban-with-coinbase-hinting-at-revolt/ ↩

-

Bank Policy Institute, "Closing the Payment of Interest Loophole for Stablecoins," August 12, 2025, and subsequent joint trades letters through May 2026. https://bpi.com/closing-the-payment-of-interest-loophole-for-stablecoins/ ↩

-

Latham & Watkins, "OCC Issues Proposal to Implement the GENIUS Act," March 11, 2026. https://www.lw.com/en/insights/occ-issues-proposal-to-implement-the-genius-act ↩ ↩2

-

Perkins Coie, "Stablecoin Interest, Yield, and Rewards: OCC Proposes Sweeping Regulations Under the GENIUS Act," March 4, 2026. https://perkinscoie.com/insights/update/stablecoin-interest-yield-and-rewards-occ-proposes-sweeping-regulations-under ↩

-

CoinDesk, "Clarity Act, in the Flesh, Unveiled by U.S. Senate Banking Committee Before Hearing," May 12, 2026. https://www.coindesk.com/policy/2026/05/11/clarity-act-in-the-flesh-unveiled-by-u-s-senate-banking-committee-before-hearing ↩

-

ABA Banking Journal, "Senate Banking Committee Advances Clarity Act," May 14, 2026. https://bankingjournal.aba.com/2026/05/senate-banking-committee-advances-clarity-act/ ↩

-

CNBC, "Crypto Industry Scores Win as Clarity Act Regulation Bill Clears Senate Hurdle," May 14, 2026. https://www.cnbc.com/2026/05/14/clarity-act-congress-crypto-senate.html ↩

-

American Bankers Association, Bank Policy Institute, et al., joint banking trades statement on the Senate Banking Committee vote, May 14, 2026. https://bpi.com/banking-trades-statement-on-senate-banking-committee-vote-to-advance-clarity-act/ ↩

Franco Di Pietro

The Payments Corner

30+ years across payments, fintech, banking, and financial infrastructure. Operator-level perspectives on the systems that move money.