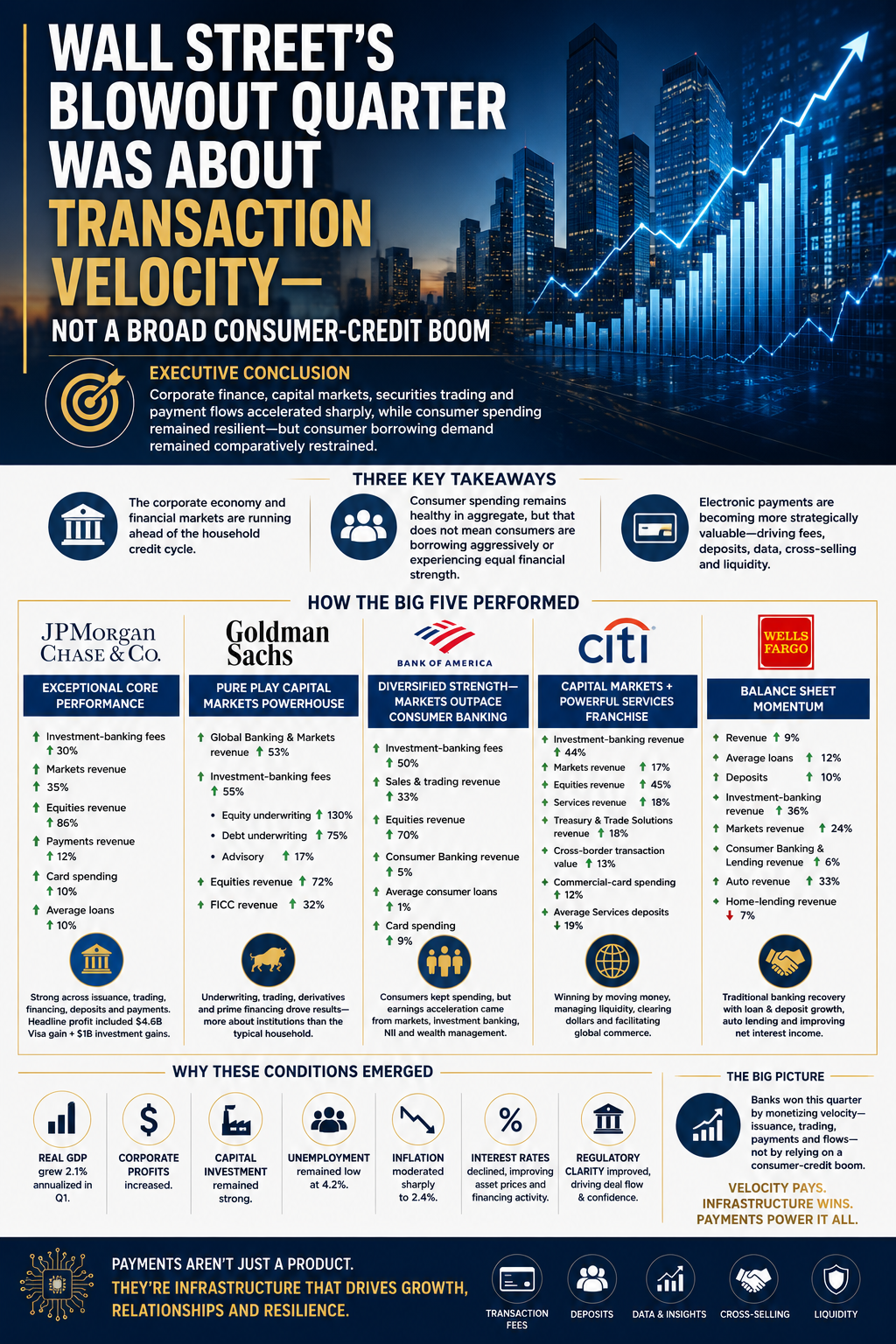

Transaction Velocity, Not a Consumer-Credit Boom

Wall Street's blowout quarter was about money moving — not consumers borrowing more. Spending is up; borrowing is flat. That decoupling is where the next few years of lending and payments strategy get decided.

Subscriber · Sign in to listen to the audio briefing

Audio briefings are available to subscribers. Sign in with the email you used to subscribe — we'll send a one-time code.

Wall Street had a blowout quarter because money was moving — not because consumers were borrowing more. Those are different economies, and the gap between them is the story.

Five banks earned roughly $49 billion in a single quarter, and the headlines read it as a strong economy. The prints said something narrower. The acceleration came from underwriting, trading, dealmaking, and payment flows — transaction velocity — not from households taking on debt. Goldman's banking and markets revenue rose 53%. JPMorgan's equities rose 86%. Strip out the movement of institutional money and the consumer chapter is quieter: spending resilient, borrowing flat.

That decoupling is the signal worth holding onto. Card spend rose roughly 10% across the majors — JPMorgan up 10%, Citi's U.S. cards up 11%, Bank of America's combined spend up 9%. Yet Federal Reserve data show revolving credit contracting, at a 4.7% annualized rate in May, with loan demand softening across cards and autos. Consumers are still transacting. They are not levering up to do it. Payment volume and credit appetite have come apart.

Two consequences follow. For consumer lending, the era of broad balance-sheet expansion is not back — precision is. Banks are competing hard for prime and affluent cardholders, growing lines selectively, and increasingly underwriting on transaction and deposit behavior rather than bureau scores alone. The consumer economy is a barbell, and it is being financed like one.

For payments, interchange is no longer the point. The transaction flow is valuable for the deposit it parks, the data it generates, the treasury relationship it anchors, and the lending it eventually cross-sells. Citi's Treasury and Trade Solutions revenue rose 18% — that is the tell. Whoever holds the payment credential increasingly holds everything downstream of it.

The banks did not report that everyone is doing well. They reported that money moved — and that the institutions positioned where it moved got paid. The question the next few years will answer is who owns the flow when spending and borrowing have stopped moving together.

#Banking #ConsumerCredit #Payments #IssuingRisk #Fintech

Franco Di Pietro

The Payments Corner

30+ years across payments, fintech, banking, and financial infrastructure. Operator-level perspectives on the systems that move money.

Related Insights

BNPL Sits Directly in the Gap Between Consumer Behavior and Traditional Credit Models

BNPL sits directly in the gap between how consumers experience credit and how institutions traditionally model it. The consumer-side behavioral pattern is consistent and well-documented. But the issuer-side value proposition is discussed far less often — even though it may be just as important.

Consumers Experience Credit Very Differently Than Institutions Model It

Most credit models assume people think in terms of credit limits, utilization, APRs, and revolving balances. But consumer behavior tells a very different story. Households experience credit through a much more immediate and practical lens — and that disconnect shapes everything from product design to underwriting logic.

HELOC Is No Longer Just a Lending Product. It's Becoming an Experience.

Most marketing mailers go directly into the discard pile. This one didn't. Aven's HELOC proposition isn't just a marketing innovation — it's fundamentally a processing innovation. A traditionally episodic lending product is becoming transactional, and that's a much deeper shift than it first appears.